OSK Strategy and Outlook (Feb 2012)

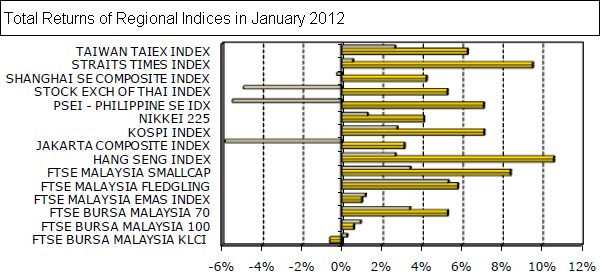

Global Rally ex Malaysia. While global markets rallied in Jan 2012 to post their best January performance since 1994, Malaysia languished as an exception among all the major markets in East Asia, thus strangely validating our Sell call on the Malaysian market in January. Globally, the economic outlook in the US remained stable with 66% of companies that reported earnings thus far beating estimates. While the situation was different in Europe with the European Financial Stability Fund (EFSF) losing its AAA rating with S&P, nonetheless, the slush of liquidity unveiled by the Long Term Refinancing Operation (LTRO) allowed European markets to rally accordingly as bond yields in Italy declined dramatically.

Takeover spare continues. While December saw the privatization offers for KFC, QSR and YTL Cement as well as rumours of Proton’s stake sale by Khazanah, January saw more of the same including:

- DRB-Hicom acquiring Khazanah’s 42.7% stake in Proton for RM5.50 a share.

- Can One acquiring a 32.9% stake in Kian Joo for RM1.65 a share

- Samling Strategic Corporation’s plans to privatise Lingui and Glenealy at an indicative price of RM1.63 and RM7.50 per share respectively.

Comeback kings. Top Gainers for January were comeback kings which had languished in

2011 but which were either driven by fundamentals (such as JCY) or rumours (such as Maybulk). Sector-wise, Tech (driven by JCY) and Transport (driven by Maybulk and MAS) as well as construction (by Mudajaya and Gamuda) gave the best returns for the month.

OUTLOOK: BETTER TO BE NIMBLY FLEXIBLE THAN DOGMATICALLY WRONG

Right but still… While we were correct in our calls for the market in Jan 2012, calling a SELL on the broad market and choosing “alternative” Buys as our Top 5 Buys for the month, still the market performed better than we had expected while global markets soared despite a patchy month of headlines. While equity markets do tend to outperform in January given the re-balancing of portfolios in a new year, the strength of the market thus far has taken us by surprise.

Be prepared for an upgrade. If indeed the KLCI performs well over the next 15 days inline with a global rally, we would be forced to rethink our bearish view for 1H12. Instead, we may upgrade our call on the market to a NEUTRAL from the current Sell, and may well promote more cyclical sectors such as Oil & Gas and Construction. While the market may subsequently turn south after a 1Q rally, still the flush of liquidity in the system may keep it resilient for most of the year. For now, we remain Defensive with Consumer stocks and other defensive mid-cap plays likely to outperform still in the short term.

Top Buys are Defensives with Good Results expected.

With February being a results seasons month, we go back to fundamentals to select our Top Buys. Four of our Top 5 “Alternative” Buys outperformed the KLCI in January, namely Sarawak Oil Palms, Supermax, JCY and Old Town. For February, therefore, our selection of Top Buys for the month of February is mainly culled from these expected defensive out-performers, namely:

- KPJ Healthcare – While results for the 4Q are typically not stellar (doctors tend to go on holidays and patients tend to postpone treatments where possible given the festive season), the excitement surrounding the upcoming listing of Integrated Healthcare Holdings could be enough to spur the share price upwards.

- Malaysia Building Society (MBSB) – We are expecting a strong set of results for the company for 4Q11 and the recent civil servant pay hike in 2012 should mean management should provide a decent enough outlook going forward.

- QL Resources – After two quarters of lackluster earnings due to poor fish catch in Sabah, we understand the catch improved in 4Q11. Also, expansion plans in Indonesia and Vietnam are largely on track.

- Media Chinese – Expecting the best ever quarterly results in 4Q11, we still see many catalysts for ad spending in 2012 including the General Elections, 2012 Olympics and Euro 2012.

- Padini – Our new Top Buy in the Consumer Retail space, a recent visit confirms that the company has an excellent profit track record, solid management, a good growth story (in the form of value fashion outlet Brands Outlet) and cheap valuations (below 10x forward PER). What’s not to like?

Source: OSK Research

Comments

Post a Comment